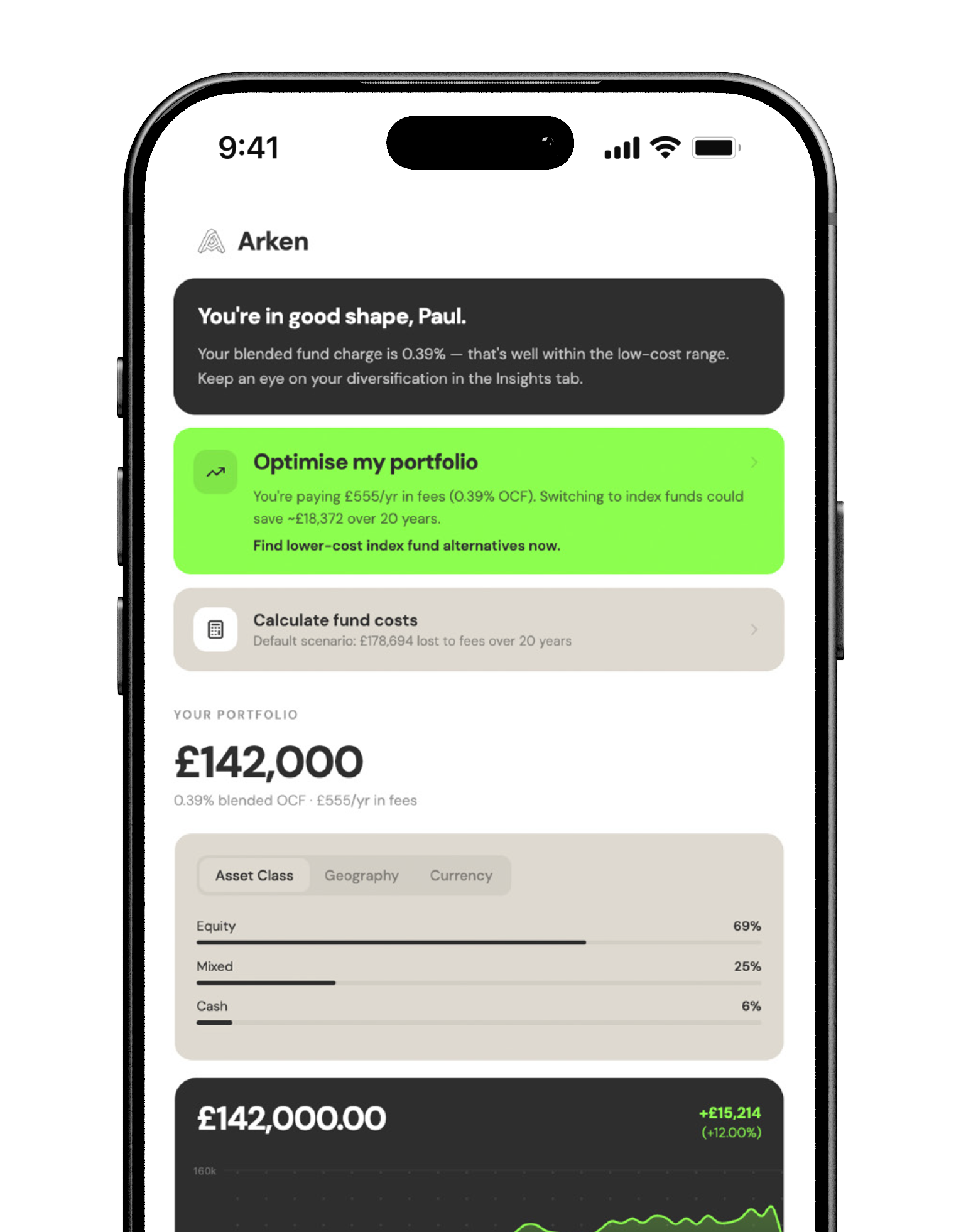

Optimise your portfolio with financial intelligence.

Most investors don't realise how much their portfolio is costing them. Hidden fees, poor diversification, and misaligned allocations quietly drag on returns.

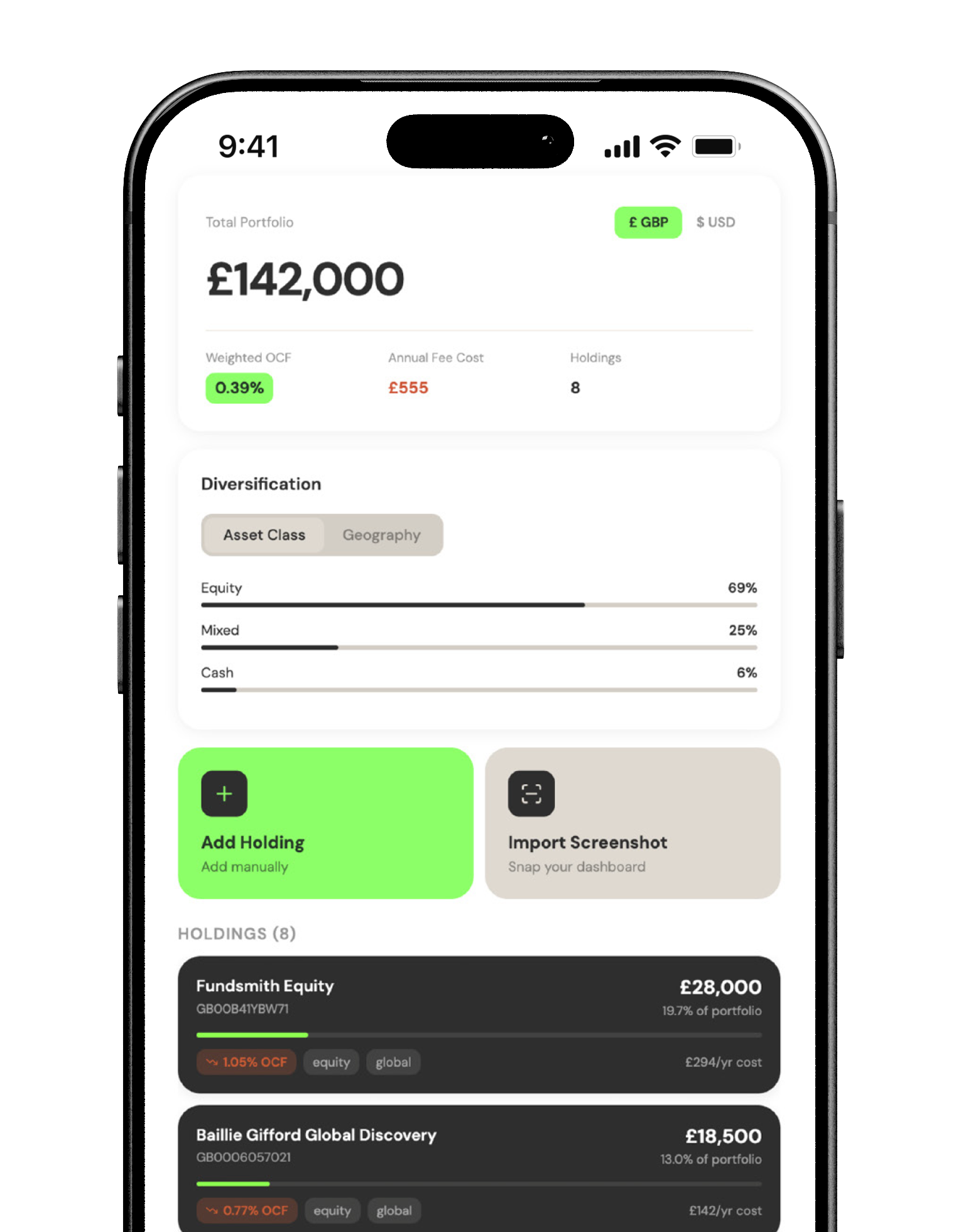

See your true portfolio exposure and performance in seconds.

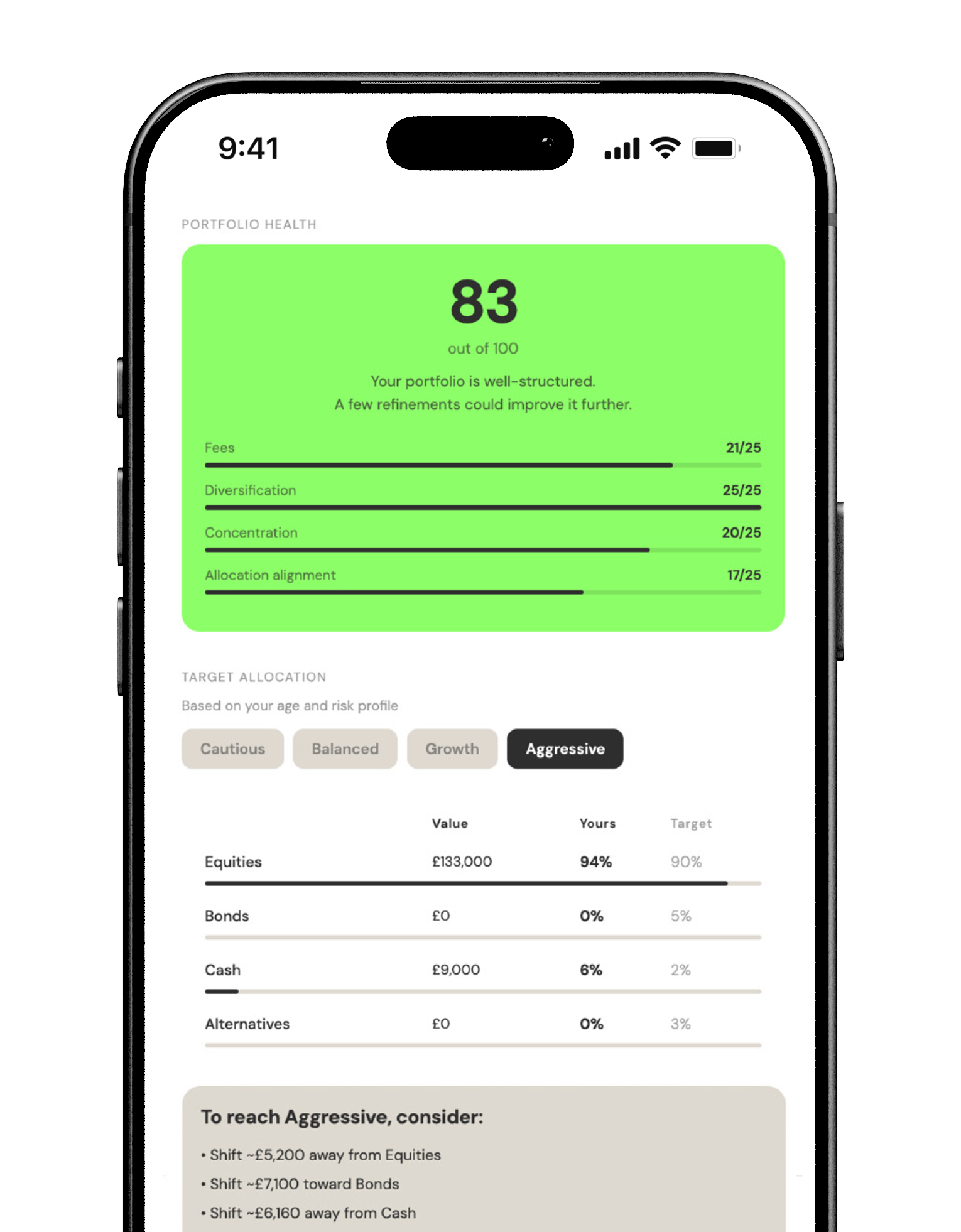

Portfolio Health Score

Scored 0–100 across fees, diversification, concentration risk, and allocation alignment. No guesswork — you see exactly what's working and what's holding you back.

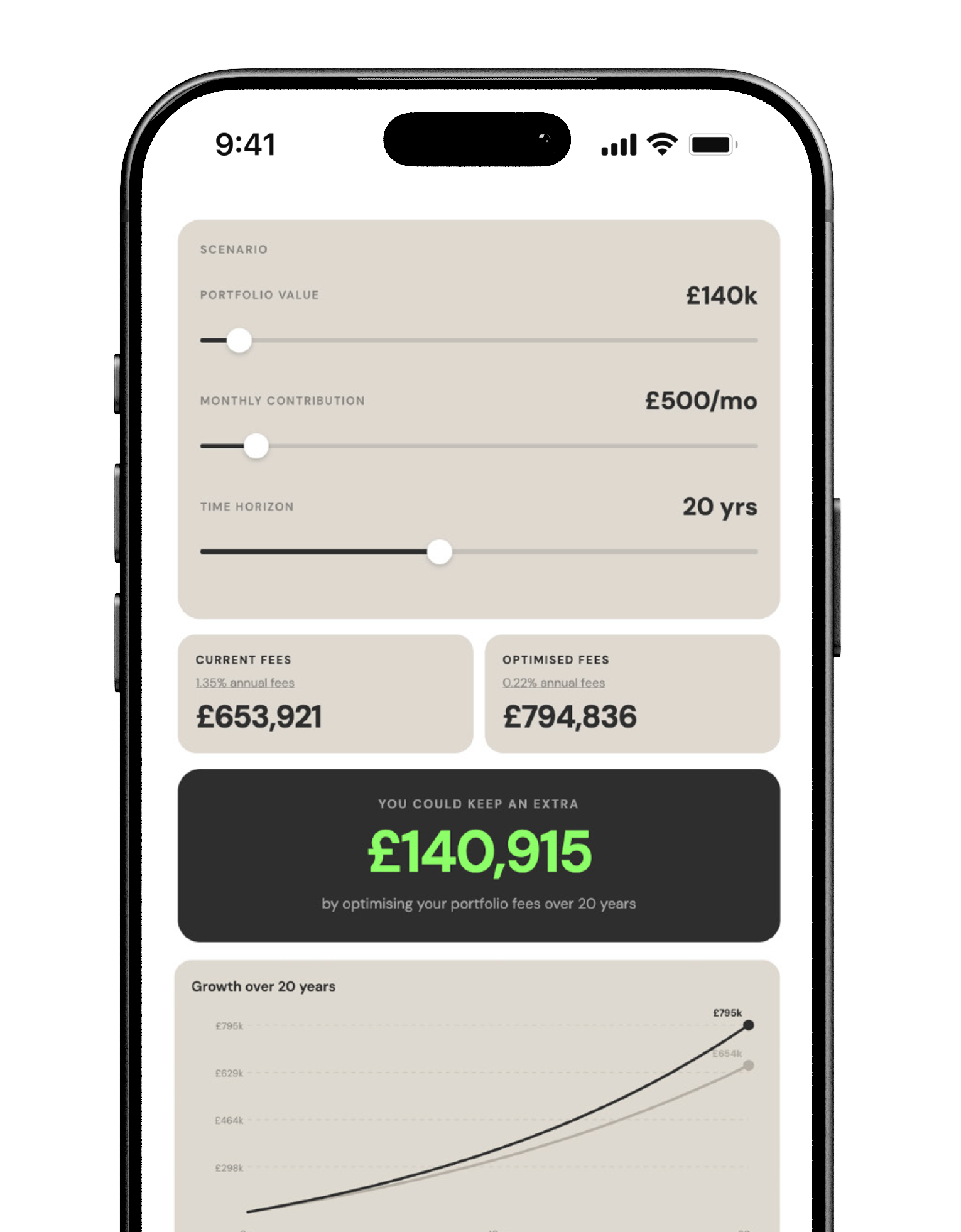

Fee Calculator

A 1.5% charge sounds small. Over 20 years it can silently erode tens of thousands of pounds. See the real cost of your current portfolio and compare alternatives.

Optimise for Growth

Arken compares your holdings against Cautious, Balanced, Growth, or Aggressive allocation models — and shows you exactly what to rebalance.

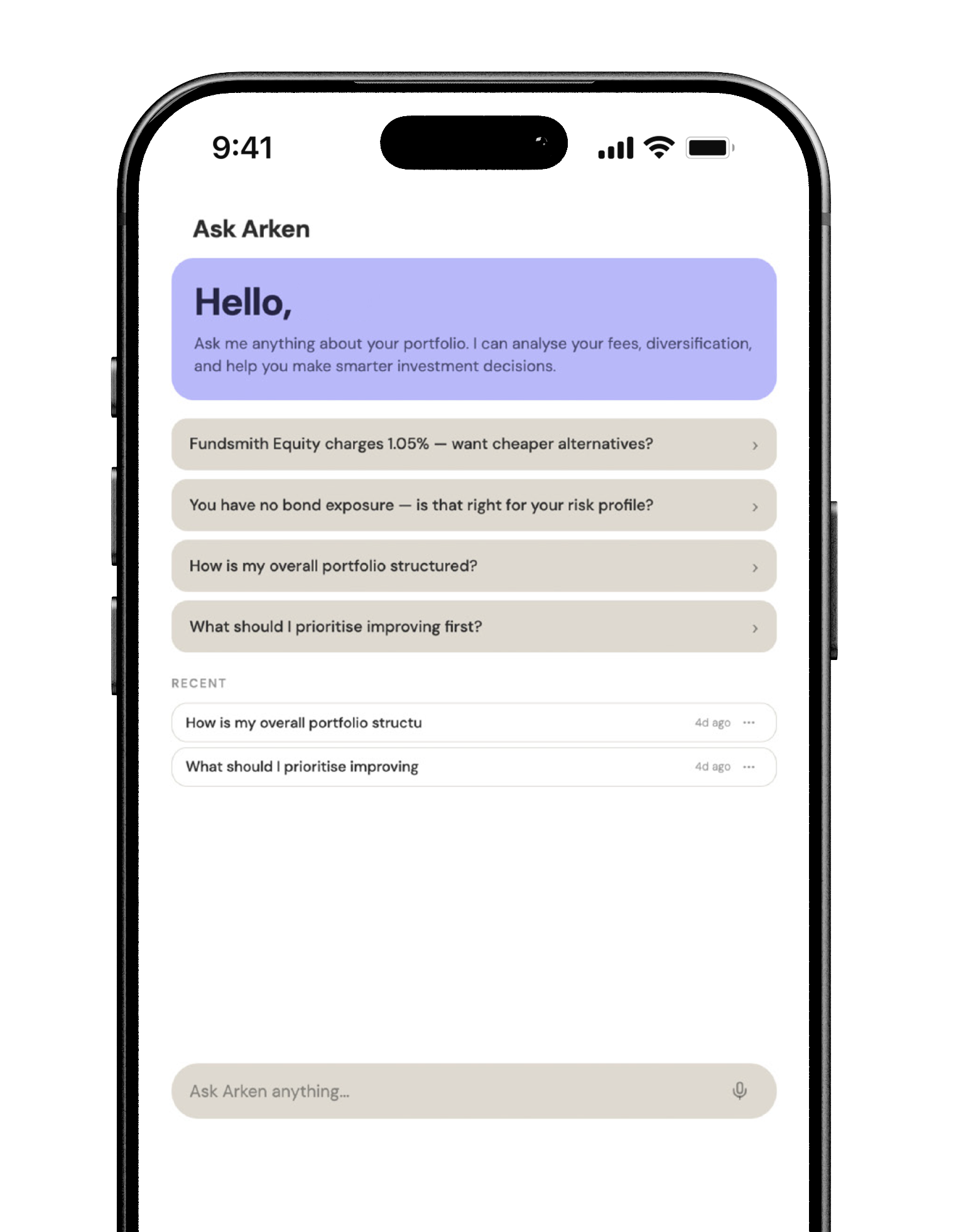

AI Advisor

Talk to Arken by text or voice about your specific portfolio. It knows your holdings, fees, and risk profile. Direct, contextual answers — not generic articles.

Arken is an educational tool. It is not regulated by the FCA and does not constitute financial advice.

UK retail investor FAQs: 25 of the most common questions answered

Practical answers to the real questions UK investors ask about portfolios, fees, risk, tax wrappers and retirement — with clear context and actionable insights.

Portfolio Health

Is my portfolio well-diversified, or am I too concentrated?

A lot of portfolios look diversified, but aren't. You might own several funds yet still be heavily exposed to the same countries, sectors, or even the same handful of companies — especially large US tech stocks.

Read moreDo I have too much US tech in my portfolio?

Probably more than you think. A lot of portfolios that look diversified are actually heavily exposed to US tech — just spread across different funds.

Read moreDo I own too many ETFs or funds?

Possibly. Owning more funds doesn't always improve diversification — it often just adds overlap and makes your portfolio harder to understand.

Read moreHow many funds should I have in my portfolio?

There's no perfect number — but most investors need fewer funds than they think.

Read moreAm I too concentrated in my portfolio?

If a small number of investments are driving most of your returns (or losses), you're probably more concentrated than you realise.

Read moreHow do I see my real sector exposure across all my investments?

You need to look at your portfolio as a whole — not just individual funds.

Read moreShould I invest more outside the US?

Maybe — many investors are already more exposed to the US than they realise.

Read morePerformance & Fees

How do I know if my portfolio is performing well?

You can't judge performance in isolation — you need context around risk, goals and time horizon.

Read moreWhy is my portfolio underperforming the market?

There's usually a clear reason — and it doesn't always mean something is wrong.

Read moreWhat's a good return for an investment portfolio?

There's no single number — a "good" return depends on your risk level, time horizon, and personal goals.

Read moreAm I paying too much in fees?

Fees compound against you every year. Even small differences add up dramatically over time. Aim for total costs below 0.5% per year.

Read moreExpensive funds vs ETFs — is the cost worth it?

Broad index ETFs are almost always cheaper and more efficient than actively managed funds for most investors.

Read moreRisk & Behaviour

Am I taking on too much risk for my investment timeline?

Your true risk tolerance is revealed when markets actually fall, not in hypothetical questionnaires. The right risk level depends mainly on your time horizon.

Read moreShould I invest a lump sum all at once or drip it in?

Lump sum investing beats pound-cost averaging about two-thirds of the time. But DCA can be better if investing everything at once would cause you to panic.

Read moreShould I sell when the market crashes, or hold?

Every major market crash has been followed by full recovery and new highs. Selling during downturns crystallises losses and often causes investors to miss the rebound.

Read moreHow much should I keep in cash versus invested?

Keep 3–6 months of living expenses in accessible cash. Money needed within 2–3 years should stay in cash. Everything beyond that should generally be invested.

Read moreShould I invest a lump sum all at once or drip it in?

Lump sum investing beats pound-cost averaging about two-thirds of the time because markets tend to rise over time. However, DCA can be better for your behaviour.

Read moreShould I rebalance? How often should I rebalance my portfolio?

Portfolios drift naturally as some assets outperform others. Rebalance annually or when any allocation drifts more than 5% from target.

Read moreISA, Tax & Wrappers

ISA vs pension — which should I use?

Both are powerful tax wrappers, but they serve different purposes. ISAs offer total flexibility. Pensions give upfront tax relief but with stricter access rules.

Read moreAm I using my ISA properly?

Use your full £20,000 ISA allowance every tax year — it does not roll over. Prioritise high-growth or high-tax assets inside the ISA.

Read moreWhat is capital gains tax and how does it affect my investments?

You pay CGT on profits from selling investments outside tax wrappers. The annual allowance is £3,000. Gains above this are taxed at 18% or 24%.

Read moreWhat is Bed & ISA and should I use it?

Bed & ISA lets you sell investments in a taxable account and immediately buy them back inside your Stocks & Shares ISA. It shelters future growth from tax permanently.

Read moreHow are dividends taxed, and how do I keep more of them?

Outside an ISA or SIPP, dividend income is taxed after a £500 annual allowance. Rates are 8.75%, 33.75%, or 39.35% depending on your tax band.

Read moreShould I consolidate my old workplace pensions?

Yes, in most cases. Consolidating multiple defined contribution pensions into one modern SIPP gives you better visibility, lower fees, and a unified strategy.

Read moreShould I invest for growth or income?

Growth and income are not opposites — total return is what matters. Younger investors usually benefit from growth-focused strategies. Those near retirement often tilt toward income.

Read moreGet clarity on your portfolio — free to download.

Arken is an educational tool. It is not regulated by the FCA and does not constitute financial advice.